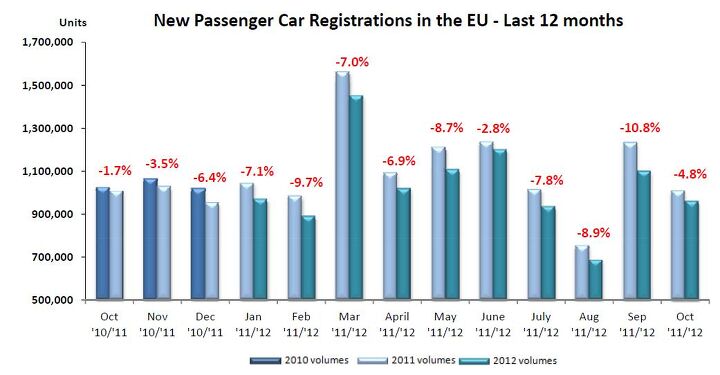

Europe In October 2012: Down Some More

The battered European new car market continues its drive into the netherworld, but the speed of descent has lowered a little. According to data compiled and released by the European manufacturers association ACEA, 959,412 passenger vehicles were registered in October, 4.8% less than in October last year. It looks like the year will end with some 12 million cars sold, a level the EU 27 hasn’t seen since it existed.

January through October, new car registrations stand at 10,327,276 units, 7.3% less in than in the first ten months of 2011.

Passenger Car Registrations EU October 2012Oct’12Oct’11YoYYTD 12YTD 11YoYAUSTRIA26,32228,909-8.9293,212302,448-3.1BELGIUM41,84642,462-1.5428,579483,008-11.3BULGARIA1,5121,729-12.615,76416,083-2.0CYPRUS7951,168-31.99,68712,194-20.6CZECH REPUBLIC15,96314,858+7.4147,022142,343+3.3DENMARK15,21612,400+22.7143,715139,630+2.9ESTONIA1,4741,335+10.414,78812,740+16.1FINLAND8,18210,070-18.797,115110,179-11.9FRANCE162,335176,103-7.81,593,8441,837,374-13.3GERMANY259,529258,253+0.52,618,3272,659,989-1.6GREECE5,1115,023+1.850,64684,254-39.9HUNGARY4,0473,511+15.343,36937,326+16.2IRELAND1,6611,566+6.178,28688,729-11.8ITALY116,875133,411-12.41,207,8601,504,528-19.7LATVIA1,001974+2.88,9968,751+2.8LITHUANIA1,1901,180+0.810,38011,136-6.8LUXEMBURG4,4543,923+13.543,54443,532+0.0NETHERLANDS26,89643,635-38.4454,273497,520-8.7POLAND22,14622,650-2.2229,209225,194+1.8PORTUGAL7,3889,137-19.181,827132,601-38.3ROMANIA6,7827,828-13.455,91063,709-12.2SLOVAKIA4,7965,751-16.658,64155,705+5.3SLOVENIA3,7384,547-17.842,44550,925-16.7SPAIN44,87357,278-21.7600,237681,199-11.9SWEDEN24,02825,052-4.1227,739252,688-9.9UNITED KINGDOM151,252134,944+12.11,771,8611,688,038+5.0EU 27959,4121,007,697-4.810,327,27611,141,823-7.3Again, there is the story of the two Europes, with the UK and some eastern countries up solidly, with Germany flat, and problem states in the south down hard. Greece is up a bit, it looks like it can’t fall much harder than a 5,000 unit month. Greece is down nearly 40 percent for the year.

Passenger Car Registrations EU October 2012OctoberJanuary – October %ShareUnitsUnits% Chg %ShareUnitsUnits% ChgOct’12Oct’11Oct’12Oct’11YoYOct’12Oct’11Oct’12Oct’11YoYALL BRANDS959,4121,007,697-4.810,327,27611,141,823-7.3VW Group25.523.9244,595240,628+1.624.723.22,553,8412,580,242-1.0VOLKSWAGEN13.312.7127,793128,481-0.512.812.31,323,8451,372,950-3.6AUDI5.95.156,51751,093+10.65.65.0582,528553,454+5.3SEAT2.12.219,86422,074-10.02.12.3213,028254,293-16.2SKODA3.93.937,15638,845-4.33.83.6395,722397,864-0.5Others (1)0.30.03,265135+2318.50.40.038,7181,681PSA Group12.312.3118,143124,435-5.112.012.71,238,6801,411,805-12.3PEUGEOT6.76.663,99766,978-4.56.56.9668,932767,632-12.9CITROEN5.65.754,14657,457-5.85.55.8569,748644,173-11.6RENAULT Grp8.810.784,783108,090-21.68.59.6874,9271,068,954-18.2RENAULT6.68.563,69085,451-25.56.67.8678,663866,434-21.7DACIA2.22.221,09322,639-6.81.91.8196,264202,520-3.1GM Group7.17.968,48179,951-14.38.28.7847,761970,668-12.7OPEL/VXH6.06.657,75866,274-12.86.87.4700,422825,590-15.2CHEVROLET1.11.410,70413,645-21.61.41.3147,078144,678+1.7GM (US)0.00.01932-40.60.00.0261400-34.8FORD7.57.872,33078,861-8.37.68.1786,989898,767-12.4FIAT Group6.66.663,25667,009-5.66.57.2672,458803,187-16.3FIAT4.94.847,14848,309-2.44.85.2490,926583,172-15.8LANCIA/CHRY0.70.86,8788,109-15.20.80.880,40686,109-6.6ALFA ROMEO0.70.86,8448,243-17.00.71.076,528110,183-30.5JEEP0.20.22,1102,038+3.50.20.221,32418,382+16.0Others (2)0.00.0276310-11.00.00.03,2745,341-38.7BMW Group6.46.261,10762,148-1.76.25.9640,165654,013-2.1BMW5.14.948,78549,248-0.95.04.7511,792518,554-1.3MINI1.31.312,32212,900-4.51.21.2128,373135,459-5.2DAIMLER5.45.051,33049,987+2.75.24.9532,894547,528-2.7MERCEDES4.74.345,24643,823+3.24.64.3473,657481,303-1.6SMART0.60.66,0846,164-1.30.60.659,23766,225-10.6TOYOTA Grp4.03.838,44238,007+1.14.23.9433,863435,997-0.5TOYOTA3.83.636,80536,195+1.74.03.7411,804415,350-0.9LEXUS0.20.21,6371,812-9.70.20.222,05920,647+6.8NISSAN3.43.232,19732,136+0.23.53.4360,602380,240-5.2HYUNDAI3.42.932,35529,162+10.93.42.9350,608321,491+9.1KIA2.82.827,10728,639-5.32.72.1277,999237,646+17.0VOLVO2.01.919,22018,758+2.51.71.8176,930198,380-10.8SUZUKI1.11.210,52712,200-13.71.21.3125,757141,349-11.0HONDA1.01.29,97012,215-18.41.11.1115,615122,217-5.4JLR Group0.90.88,6567,734+11.91.00.7101,41978,549+29.1LAND ROVER0.80.67,2586,206+17.00.80.581,82259,266+38.1JAGUAR0.10.21,3981,528-8.50.20.219,59719,283+1.6MAZDA0.70.86,3658,037-20.81.01.098,912114,203-13.4MITSUBISHI0.60.75,2817,117-25.80.60.858,84087,859-33.0OTHER0.50.35,2672,583+103.90.80.879,01688,727-10.9On the OEM side, Volkswagen Group continues to win the war of attrition. Its sales are up 1.6 percent for the month, and down only 1 percent for the year. More than a quarter of all cars sold in the EU in October came from the Volkswagen Group. After that, a bloodbath. Renault down 21.6 percent, GM down 14.3 percent Ford lost 8.3 percent, Fiat down 5.6 percent in October, an all of them down double digits for the year.

Continuing to drive Europeans crazy: Hyundai, up 10.9 percent in October. Sergio Marchionne implores the EU to keep the Koreans out, Hyundai smiles, knowing that most of its cars sold in Europe are made in Europe.

Bertel Schmitt comes back to journalism after taking a 35 year break in advertising and marketing. He ran and owned advertising agencies in Duesseldorf, Germany, and New York City. Volkswagen A.G. was Bertel's most important corporate account. Schmitt's advertising and marketing career touched many corners of the industry with a special focus on automotive products and services. Since 2004, he lives in Japan and China with his wife <a href="http://www.tomokoandbertel.com"> Tomoko </a>. Bertel Schmitt is a founding board member of the <a href="http://www.offshoresuperseries.com"> Offshore Super Series </a>, an American offshore powerboat racing organization. He is co-owner of the racing team Typhoon.

More by Bertel Schmitt

Comments

Join the conversation

Yep, Europe is in a recession and the Euro squabbling doesn't help any.

JLR would be up by more than 30% if it wasn't for the fact they are running out of capacity