Mitsubishi Motors: And Then There Were…

In April, when they released their FY2013 annual results, MMC (Mitsubishi Motors Corp) reported record profits; see Reuters and Automotive News for stories.

Don’t get too excited.

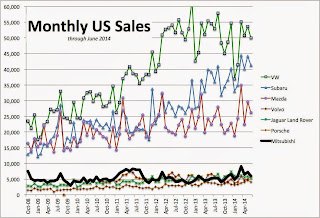

Mitsubishi Motors’ North American operations are struggling; MMC sells far less than any other Asian car company in North America. The next smallest, Mazda, sold almost three and a half times as many vehicles in April 2014. Only six firms sold fewer cars, and of those only Volvo is not a niche luxury marque. (The other five, in decline order of sales, are Jaguar/Land-Rover, Porsche, Tesla, Maserati and Ferrari.)

There are positive signs, with April sales up 46.6% over 2013 and year to date sales up 29%. Only Maserati had a larger increase, but they sold 753 vehicles last year, so that shift represents only a few additional cars. On the other hand, among manufacturers building cars for mainstream customers, Mitsubishi sells the least, so its percentage increase likewise represents only a modest absolute change. Nevertheless Mitsubishi has been improving its North American operation, with net sales up 53% from 2012 to 2013.

Such sales however mean that MMC’s Illinois plant – begun in 1988 as Diamond-Star during the era when Chrysler was a major shareholder – continues to operate in the red. Whether or not Mitsubishi will be able to mount a comeback from the brink of essentially complete failure in North America will depend heavily on the continued expansion of their share and the overall vehicle market. Summer sales are expected to be substantial enough to grow the car market in 2014 over 2013, but that increase won’t be enough to float MMC. Mitsubishi will likely see its sales cannibalized by the other automakers and go the way Suzuki, Isuzu and Daihatsu, Japanese firms that have completely withdrawn from North America. Ultimately it may prove a Saab story.

But their problems aren’t just the US. They’ve pulled out of production in Europe, selling their Nedcar facility. They’ve just restructured debt with their four main creditors – and largest shareholders – who took an average 25% haircut on their preferred shares, to the tune of ¥95 billion (US$950 million). [This is made clear only in their Japanese-language filings.] Perhaps MMC’s shareholders want a tax writeoff and figure their last bailout won’t be recouped. But it also provides MMC with a clean ownership structure that would make a sale easier. Whether anyone would want to buy them is less clear: the company has a stormy history that includes 2 failed sales and an unenviable strategic position. They aren’t unique in this; many other small firms have failed or changed hands in the past half dozen years. But my guess is they’re more likely to provide a Saab story than any of the other Japanese bit players.

Mitsubishi Motors’ origins saddled it with an inefficient structure. During World War II Mitsubishi Heavy Industries (MHI) made munitions ranging from warships to the Zero fighter. After 1945 the US Occupation split up the firm into 3 pieces, each of which made different sorts of motor vehicles – three-wheeled cars, scooters, commercial trucks – as they struggled to find things to sell in the grim 1940s and early 1950s. After the Occupation ended MHI’s former pieces merged. The end result was the Mizushima plant in western Japan producing minicars (“kei” cars), Okazaki in central Japan making passenger cars, and Maruko in Tokyo (eastern Japan) making trucks, all within the larger MHI with its industrial machinery, shipbuilding and heavy equipment operations.

Then along came Chrysler, wanting to source small cars in Japan to provide dealers with something to compete against the VW Beetle, which in 1968 sold 600,000 units in the US. (Ford and GM did the same thing, eventually ending up with controlling stakes in Toyo Kogyo – renamed Mazda to echo its brand – and Isuzu.) In 1970 MHI bundled together the three automotive pieces into MMC and set it up as an independent company, with Chrysler to take a 35% stakeholding (which under Japanese corporate law would give them veto rights and hence de facto control). But Chrysler entered one of its periodic crises and couldn’t raise the cash, leaving it with a 15% stake in an unwieldy company. MHI and its bankers remained as the dominant shareholders. While MMC and Chrysler set up Diamond-Star, a joint venture assembly plant in Illinois that opened in 1988, by 1991 Chrysler had sold its share in MMC and various joint ventures.

[An aside: Chrysler purchased its stake in direct contravention to Japanese industrial policy of preventing foreign ownership in the industry – when push came to shove the Ministry of International Trade and Industry (MITI, now MEXT) lacked the clout to make such policies stick, cf. IBM’s operations in Japan.]

Then in 2000 DaimlerChrysler bought into MMC, eventually holding 37.5% of the company. But MMC performed poorly, not helped by Daimler’s management, and by 2004 that stake was sold off, with Daimler keeping MMC’s truck division, Fuso, the one piece that made strategic sense for its Asian production base and array of drivetrains.

In the background is a rollercoaster history of a piece with Chrysler. The initial spinoff from MHI coincided with the success of the Galant passenger car in Japan, alongside a good position in the growing “kei” market and in the heavy truck and bus market – which by the way meant that the 3 original production bases remained fiefdoms. MMC then entered the US market, as did the partners in the other Detroit Three alliances. Unlike Isuzu and Mazda, both of which ceased production in the US, MMC has yet to shutter its plant in Illinois, despite low capacity utilization and poor North American sales. Inside Japan sales did well during Japan’s bubble, with MMC introducing new brands, including the luxury Diamante. Again, given the bubble context, that didn’t go well. Next MMC rode the sport utility boom with the Pajero, its Jeep-like product. It was the first firm to do so in Japan, and until rivals entered it earned a lot of money.

Meanwhile it expanded overseas, with assembly plants not just in the US but also NedCar in Europe (from 1991), Chrysler’s old operation in Australia (from 1980), a tie-up with Proton in Malaysia, an engine and later transmission plant and CKD operation in the Philippines, and stand-alone operations with a proper assembly plant in Thailand. Finally, on an ad hoc basis MMC also exported plant and equipment to various firms, including Hyundai and Proton.

Most fared poorly. Its domestic bubble-era brands are gone, as are NedCar (closed in 2012) and Australian (2008) operations. Domestically it turned out a bit over 500,000 vehicles in 2013, but 60% of those were exported. With the yen weak (today at ¥101 per US$) exports are now profitable. Exports are also the focus of their US operations, which currently turn out 70,000 SUVs a year. But exports are an expedient, not a strategy, only grasping at a short-term profit source. Meanwhile, 60% of domestic sales are of minicars. That’s good news, because sales of that segment are rising (up 10% over the last year) but it’s also bad news, because low-priced cars cannot possibly generate the profits needed to keep the company going.

International operations look better, centered in Thailand with joint ventures in China and Russia. In terms of production they are the same order of magnitude as MMC’s domestic operations. But because most of domestic production is exported, the international-to-domestic sales mix is closer to 90:10 than 50:50. What has tided the company over domestically were one-off OEM deals with Nissan, Honda and others. But again, that’s a temporary expedient; there’s no history in the auto industry over the past century, in the US or elsewhere, of sustained interfirm trading. Much more solid are its pickups in Thailand and SUVs in other developing markets such as Russia and China.

Jan-May 2014changeDomestic Production273,429+41%Domestic Sales62,954+14%Regular Cars21,376-19%Kei Cars29,708+104%Commercial Vehicles11,870-16%Exports147,190+12%Overseas Production257,781-5%Total Production531,210+14%Domestic Sales/Total Production12%In Japan, Europe and North American its dealership networks remain weak. For example, in Japan it was late to expand into urban areas, and so had poor locations and poor franchisees. In order to finance its urban presence MMC resorted to supplying cash in turn for equity stakes in dealers. It then dispatched managers from the manufacturing side, who have not proved adept at selling cars – Tesla be warned! In North America and Europe it is hampered by years of poor sales and an uncertain product strategy. (TTAC product reviews of the Mirage and Outlander are less than stellar, while noting the lack of a clear lineup.) Only repeated infusions of equity from the Mitsubishi family of companies kept it afloat, and 25% of those have now been written off.

Thus MMC is a firm with a strong presence in Southeast Asia; it’s basically a Thai firm with lots of engineering facilities and a few underutilized factories in Japan. It has modest operations in China, though as typical of late entrants its factories are scattered from Manchuria to Guangzhou. Then there’s a production base in Japan. Its product lineup is good for the developing world, but in 3 of the 4 largest markets – North America, Europe and Japan – its product mix is weak. The company is thus claiming it will ride emerging market dynamism to success. Elsewhere – in developed markets – its proclaimed focus is electric vehicles, to me a dim idea. But where will it be able to generate profits sufficient to sustain its engineering operations and factories in Japan? Exports only work while the yen remains weak. And without a steady stream of new products, all facing the expensive engineering challenges of increasing demands for fuel efficiency, low emissions, safety and connectivity, it can’t survive.

So selling the firm strikes me as their last straw. There’s a problem: for whom would a purchase make sense? Its current alliances with Nissan-Renault make that a possible option, as they can potentially use MMC’s plants (though not its dealers) in the US and Japan). Perhaps a Chinese company can be tempted, as with PSA and Volvo. But as I see it, FiatChrysler is the one global player with a footprint in North America and Europe that lacks a strong presence in China and developing Asia, the regions where MMC is least weak. If so, this would be the third attempt involving some iteration of Chrysler. But remember, three strikes and they’re out. And that will be MMC’s fate, if it can’t sell itself before the yen again strengthens.

To reiterate: I believe they’re more likely to be a Saab story.

N.B. This draws upon a post by my student, Anton Reed W&L’14 in May 2014 for Economics 244. The Prof edited it and appended the global story.

Mike Smitka is an economist at Washington and Lee University in Lexington, Virginia. He's been a judge of the Automotive News PACE supplier innovation awards since they began in 1994. His household's vehicles are a 2014 Chevy Cruze, a 2013 Honda CR-V and a 1988 Chevy pickup. Find his auto industry course at <a href="http://econ244.academic.wlu.edu/">Econ 244</a>; he also blogs with David Ruggles at <a href="http://autosandeconomics.blogspot.com">Autos and Economics</a>.

More by Mike Smitka

Comments

Join the conversation

There are too many carmakers in Japan. I would expect no more than three will be left standing within the next 20 years.

Isuzu has only sold heavy commercial vehicles in Japan for more than a decade. The only manufacturers that might not be around in 20 years are Mitsubishi and possibly Mazda. Subaru isn't going anywhere except maybe being completely swallowed by Toyota.