Bailout Watch 59: George F. Will Votes Nay

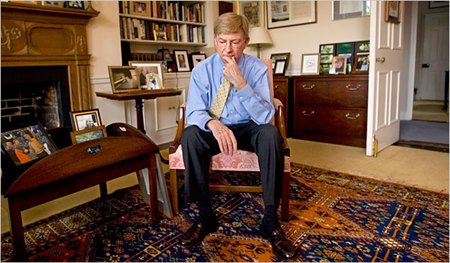

Well he would, wouldn’t he? As usual, George F. Will takes his sweet time getting to the meat of the matter: his final position on Uncle Sam’s $25b low-interest loans for The Big 2.8. And when he does, Will’s irony meter pegs out at 10. “Lemon socialism — the subsidization of the weak — is supposedly needed lest a U.S. automaker file for bankruptcy, causing the sort of civil disorder and social chaos that accompanied the disappearance of Studebaker, Packard, American Motors and others.” Will’s summation hedges his rhetorical bets, but the message couldn’t be any different from Washington Post stablemate and nominal car critic Warren Brown. “Detroit says, correctly, that some of its problems stem from fuel economy and other mandates imposed by the 535 automotive engineers on Capitol Hill. But that is beside the point, which is: No one thinks that the failure of an auto manufacturer would pose systemic risk to the economy. Americans would just buy a different mix of cars.” In fact, day after day, month after month, year after year, they already are. [thanks to loads o’ folks for the link]

More by Robert Farago

Comments

Join the conversation

How the Democrats Created the Financial Crisis: Kevin Hassett "The problem was that the trillions of dollars in play were only low-risk investments if real estate prices continued to rise. Once they began to fall, the entire house of cards came down with them. Turning Point Take away Fannie and Freddie, or regulate them more wisely, and it's hard to imagine how these highly liquid markets would ever have emerged. This whole mess would never have happened. It is easy to identify the historical turning point that marked the beginning of the end." http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aSKSoiNbnQY0

On the values, it would seem to me that the proper valuations used to be there, and that has somehow changed. I don't know exactly how it's done now, but I suspect that somewhere the likelihood of a default is mixed into the formula. As you say, the likelihood of a subprime default is extremely high, and the more of them in a given area, the higher the risk of a domino effect. I would have put the value of a subprime california loan at pennies, while one in Aspen might be worth near face value. If the loss reserves would be extreme, then GOOD! That's where we went wrong, is it not? This should have never gotten this big because only private players should have been able to play in the markets due to the risks. If someone offers you a pig in a poke, you won't buy it. How come the SEC and others allowed companies to buy dozens of supersized 5,000 pig sized pokes and put them on their books as if they had just bought 5,000 prize pigs rather than a bunch of feral cats? If the officers of Jared Jewelry put a bag of paste on their books as gemstones, they would be prosecuted. It's FRAUD. If you run Lehman, how do you claim you didn't know? If you are that stupid, don't you have a fiduciary duty to resign? Let's be gracious. Leave them each 3 million, and take the rest. Bail out the company, but weed out the so called leaders. Sorry about the rant, but I am still pissed.