How Did Autos Fare In The US Economic Recovery?

I’m an economist, and do more than think about the industrial organization (IO: “structure, strategy, conduct and performance”) of the auto industry. Here I present overall employment data and then focus on the automotive component. For a recent item on inflation and interest rates see here at my blogspot blog, Autos and Economics.

We’re now in the 6th year since the bottom fell out of the economy in 2008. Since then we’ve had monetary policy that in past environments would be considered strong stimulus. However, with no inflation, zero interest rates don’t do much, and with lots of people underwater on their mortgages – almost everyone is upside-down on their car loan, particularly as we now see 96-month-terms – well, it is powerless. Then there’s the fiscal front. State and local governments have cut employment, and that’s important, because public schools are far bigger employers than the federal government (if government is a leviathan, then it’s children who feed it!). At the Federal level we had a modest stimulus package in 2009 with the ARRA, but it was smaller than cutbacks at the state and local level, and since then federal employment is also down. So when push comes to shove, Washington believes in keeping its hands off of the economy.

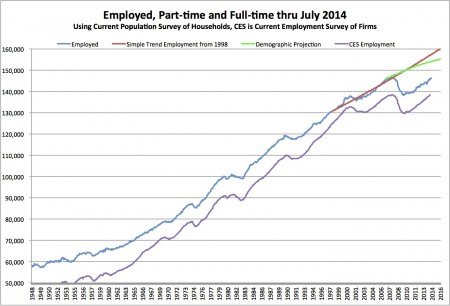

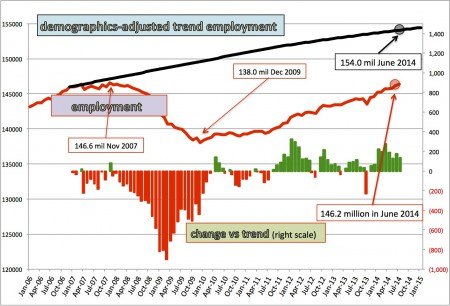

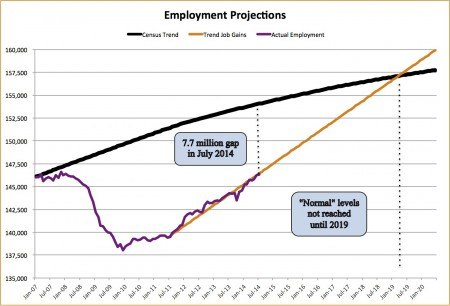

So how have we done? Here are 3 graphs that tell the overall story. (Click on them to enlarge so that you can see the details. Read the text if you believe I can convey the essence of three pictures in less than 1,000 words.)

First, when we look at the US economy over the long haul, the Great Recession stands out against all of the post-1948 era for which good-quality employment data are available. Second, the onset of the recession was very sharp, and the recovery muted relative to underlying population growth. That’s true even when I correct for baby-boomer retirements. (As a college teacher, I see thateven good students from my nationally top-15-ranked school have great difficulty in finding jobs.) Third, there’s the speed of recovery. Now my correction for baby boomer retirements suggests that we don’t need as strong job growth as in the past to keep up with population growth, but at present we’re still roughly 7.7 million shy of where ought to be. (We’re 9.2 million shy if we factor in the large number who are working part-time because they can’t find full-time jobs.) So as a true practitioner of the dismal science, looking forward suggests we won’t really be back to normal for another 5 years, assuming of course that nothing goes wrong in the interim.

Why the slow adjustment? Those in the auto industry ought to understand the dynamics when the object at hand is a durable good. A boom leads to more cars in the total fleet – my own back-of-the-envelope calculations find that during the bubble years, the total fleet should have expanded by about 12 million vehicles, whereas it grew by 22 million (to 250 million in the US). That’s a 10 million unit overhang. Erasing that required years of depressed sales – for a while new vehicle sales were actually below the scrappage rate, and not just the population growth rate. (Cash-for-clunkers helped a bit, though most of the effect was to pull sales forward.)

However, cars are short-lived compared to houses, and so a much longer housing bust (and a bigger price swing) is required to offset a boom. That’s been accentuated by the low rate at which younger Americans have been able to launch their careers, so new household formation is down. (As an example, my son lived in our house until he was 29.) Now at some point that will normalize, as the excess inventory gets worked off. There’s the equivalent of clunkers, too, as housing built in unattractive locations are permanently abandoned and torn down. (It also takes people who are underwater on their mortgage longer to recover than people who are upside-down on their car loans.) At present, new residential construction remains half of peak. I could be wrong – I hope I am! – and housing price increases and employment growth will produce a virtuous circle with accelerating employment growth. Bets, anyone?

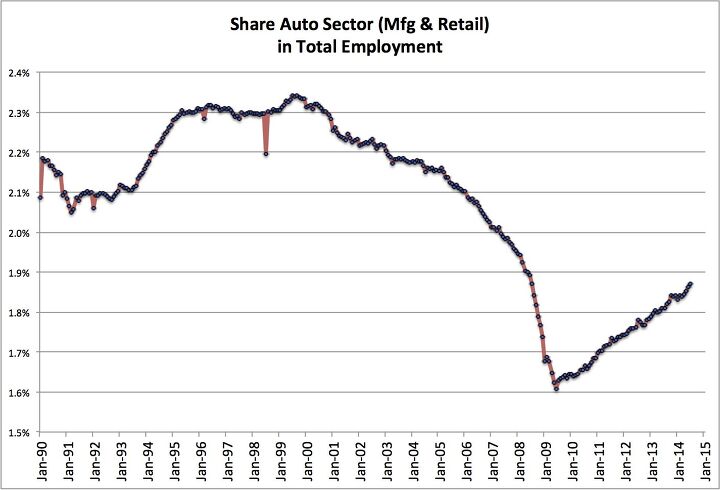

The good news is that in all this the auto industry has done pretty well. We had a gradual decline in industry jobs from 2000-2006, partly due to imports of parts and vehicles, and partly because of productivity increases, such that we simply needed fewer people. (That story holds for manufacturing on a global basis – while China employs a lot, output there has gone up even more, and their day of employment declines is close at hand.) Then came the Great Recession and employment collapsed, in retail and not just manufacturing.

For the past 4 years, however, the auto industry has been a bright spot, with job growth outpacing the overall recovery, adding 485,000 jobs. The industry picked up 0.3 percentage points of aggregate employment, and 535,000 if I add in employment at gas stations. Now make no mistake: prior to the Great Recession the motor vehicle sector accounted for 3.0 million jobs. We’re still 260,000 shy of that level, split between manufacturing and retail.

But there are jobs, and lots of new technology and new manufacturing processes to play with, and great product to market. And drive. All of us connected to the industry should be thankful.

Mike Smitka is an economist at Washington and Lee University in Lexington, Virginia. He's been a judge of the Automotive News PACE supplier innovation awards since they began in 1994. His household's vehicles are a 2014 Chevy Cruze, a 2013 Honda CR-V and a 1988 Chevy pickup. Find his auto industry course at <a href="http://econ244.academic.wlu.edu/">Econ 244</a>; he also blogs with David Ruggles at <a href="http://autosandeconomics.blogspot.com">Autos and Economics</a>.

More by Mike Smitka

Comments

Join the conversation

Mike, a very good read. I also think the US job market is changing more so than you put forward. There are many mature workers who have gone down a rung or two financially and don't have the opportunities to rise again. There just isn't the employment available. I have read much on the diminishing American middle class. Now is the time to introduce a decent minimum wage like we have in Australia. There is too much opposition to this in the US. The doubling of the minimum wage would increase the size of the American middle class. The fear is people will pay more for goods and services, which is true. But the benefits will outstrip the rise in the cost of goods and services. The benefit will be the current middle class income would also rise, but not proportionally with the minimum wage.

I believe the auto industry is a classic "leading indicator" and that the middle class always lags the wealthy in recovery.