Feds Primed To Shoot Down Some Sub-Prime Loans

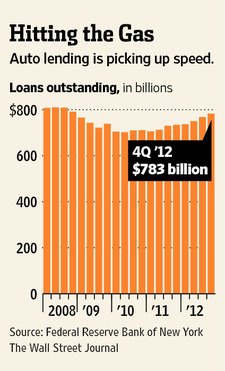

The volume of car loans is near pre-carmageddon levels, but a federal probe of business practices threatens to “slow the booming car-loan industry,” the Wall Street Journal writes.

According to the report, the Consumer Financial Protection Bureau (CFPB) has issued subpoenas to U.S. auto lenders over the sale of extended warranties and other financial products.Meanwhile, the Justice Department is looking into auto dealerships that make their own loans to customers with poor credit and charge higher rates.

Says the Journal:

“Any new restrictions could affect millions of Americans who use loans to buy new and used vehicles each year. Add-on products, such as extra insurance, are a popular mechanism used by car dealers to boost profits.”

Though such products are legal, regulators are probing whether terms and prices are adequately disclosed. The CFPB has pursued a similar strategy with credit-card companies, fining them over the use of deceptive marketing practices to sell products like identity-theft protection.”

Roughly three-quarters of all new-vehicle purchases are financed or include add-on products, the National Automobile Dealers Association (NADA) told the Wall Street Journal.

Outstanding auto loans totaled $783 billion at the end of 2012, the most in nearly four years, says the Federal Reserve Bank of New York.

Bertel Schmitt comes back to journalism after taking a 35 year break in advertising and marketing. He ran and owned advertising agencies in Duesseldorf, Germany, and New York City. Volkswagen A.G. was Bertel's most important corporate account. Schmitt's advertising and marketing career touched many corners of the industry with a special focus on automotive products and services. Since 2004, he lives in Japan and China with his wife <a href="http://www.tomokoandbertel.com"> Tomoko </a>. Bertel Schmitt is a founding board member of the <a href="http://www.offshoresuperseries.com"> Offshore Super Series </a>, an American offshore powerboat racing organization. He is co-owner of the racing team Typhoon.

More by Bertel Schmitt

Comments

Join the conversation

Speaking of add-ons... Was just at a Honda dealer looking at new accords. The dealer had a $495 charge for a TrueCoat like product applied to the car. I told the salesman I didn't want it and he said "sorry, it's already on there, you have to take it if you want to buy the car". It really bugged me to the point where I just walked away. Note: This same car also had $400 nitrogen filled tires and a $195 pin stripe. Talk about pure profit! I'm sure he would have hit me up for something else later in the process.

I remember a few years ago, a black dude had a large chain of dealerships in the States(more Eastern then West,I think) specializing in sub-prime,new buyers,and young people trying to establish credit and just starting work...His idea,and it was a good one ,was that if the weekly or bi-weekly payements weren't made,the cars were wired up and if the right codes weren't inputted,they wouldn't start........I remember most customers were quite happy with the setup and noted it was ,in a lot of cases,their only option to get a vehicle......He ended up getting sued(of course) and the claiment was probably "helped" by some rights group or the other....I don't remember the outcome,but I'm sure someone here will remember the guys name and outcome of the lawsuit.