Bailout Watch 569: Exit Strategy? What Exit Strategy?

Next up in today’s series “Selections from the GAO report on the auto bailout which closely resemble TTAC editorials of a year ago” we have the report’s discussion of a possible exit strategy. Or rather, the report’s disclosure that there’s so not an exit strategy it hurts. From the report’s conclusions:

While Treasury has stated that it plans to review all possible options for divesting itself of its ownership interest in Chrysler and GM, Treasury officials have focused primarily on an IPO for GM, both in our discussions with them and in their public statements. However, given the complexity of the economy and the financial markets, considering all of the options in the context of the companies’ financial progress and current financial conditions will be important for Treasury. The past year has indicated the extent to which a company’s financial situation can change within a period as short as a few months. Given the fluidity of conditions and the number of factors that will need to be considered when determining how and when to divest, it is important that Treasury identify the criteria it will use to evaluate the optimal method and timing for selling the government’s ownership stake. Determining when and how to divest the government’s ownership stake will be one of the most important decisions Treasury will have to make regarding the federal assistance provided to the domestic automakers, as this decision will affect the overall return on investment that taxpayers will realize from aiding these companies

Notice the use of future tense to describe these decisions? Not only is there no plan, there’s also no timeline and precious few staff to implement it. More importantly, there’s not much of a chance of a divestiture plan succeeding under any circumstances. Oh, and plenty of potential for unintended consequences. Hurray!

In the event that the companies do not return to profitability in the time frame Treasury has projected, Treasury officials said that they will consider all commercial options for disposing of Treasury’s equity, including liquidation.

Voldemort! The “L” word gets dropped by way of an explanation that Treasury is obligated to maximize taxpayer value. In other words, there’s no way to sell GM or Chrysler stakes now, thanks to the distinct lack of turnaround sales- and profit-wise. So what is the timeline? After all, you can’t have a timline without a plan, can you? Or is it the other way around? The only indication of a hard timeline is the expiration of GM’s escrow account (the final, post-bankruptcy $30b) on June 30, 2010. Which helps explain why we’ve been hearing June 2010 mooted as a GM IPO date. But who will tell Treasury when it’s really the right time to sell?

When Treasury was heavily involved in the restructuring of the companies, Treasury’s auto team consisted of 12 professional staff and 4 administrative staff, and it used the services of investment banking, consulting, and law firms. Since those agreements have been finalized and the workload has declined, two-thirds of the original professional staff has left, leaving Treasury with 4 of the original professional staff dedicated to auto issues, other OFS staff who have also helped monitor these investments, and limited use of investment or industry consultants. The leader of the auto team, who also serves as a senior adviser to the President on the auto industry, was recently appointed Senior Counselor for Manufacturing Policy, requiring him to split his time between the auto team and his new role.

Moreover, Treasury officials told us that there will likely be additional staff reductions in the future because they plan to disband the auto team over time as other OFS staff assume the role of monitoring the financial condition of the companies. In commenting on a draft of this report, Treasury officials stated that in light of recent and expected staff turnover, they are prepared to hire personnel from within Treasury or externally to fill Treasury’s monitoring function. Nonetheless, given the wind-down of the auto team— and the associated loss of dedicated staff with industry- and company-specific knowledge and expertise—we are concerned that Treasury may not have sufficient expertise to actively oversee and protect the government’s ownership interests, including determining when and how to divest these interests.

Plus:

In general, Treasury has faced challenges hiring the full complement of staff necessary to administer the TARP programs, in part because qualified candidates can often find a more competitive salary with a financial regulator, which has the authority to establish its own compensation programs without regard to certain requirements applicable to executive branch agencies… Treasury provided us with a document showing the current and projected number of staff working on AIFP, but this document did not show how Treasury determined the appropriate number of staff or areas of expertise that would be needed for future workloads.

And they need the staff. After all, if IPOs were easy, it would still be 1997 (and GM and Chrysler would have “dot com” behind their names).

Although Treasury officials said they plan to consider all options for selling the government’s ownership stakes in Chrysler and GM, they noted that they believe the most likely scenario for GM is to dispose of Treasury’s equity in the company through a series of public offerings. Treasury has publicly discussed the possibility of selling part of its equity in the company through an IPO that would occur sometime in 2010. However, by publicly discussing a method and a time for a sale of GM shares now, the extent to which Treasury is using the indicators to inform method and timing decisions is unclear. Moreover, two of the experts we spoke with said GM might not be ready for a successful IPO by 2010, because it may be too early for the company to have demonstrated sufficient progress to attract investor interest, and two other experts noted that 2010 would be the earliest possible time for an IPO. For Chrysler, Treasury officials noted that the department is more likely to consider a private sale because its equity stake is smaller, and several of the experts we interviewed noted that non-IPO options could be possible for Chrysler, given the relatively smaller stake Treasury has in the company (9.85 percent, versus its 60.8 percent stake in GM) and the relative affordability of the company.

And though the GAO doesn’t hint at how “affordable” this no-longer distressed equity would be when it hits the market, they are clear that:

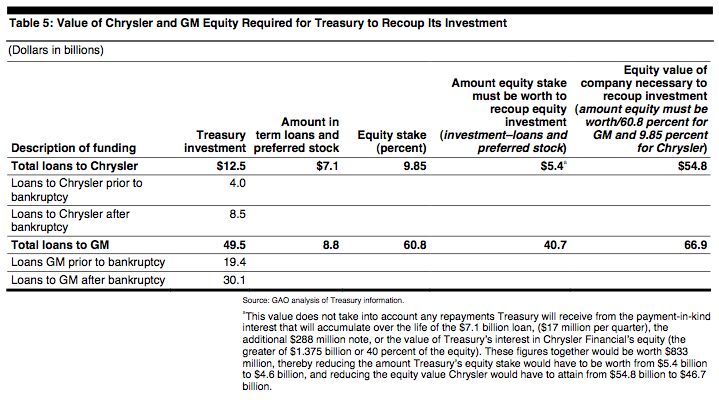

Regardless of the sales strategies used, the companies will have to grow substantially in order to reach values at which Treasury would recover the entirety of its equity investment upon sale of its equity, which Treasury and others consider to be unlikely. On the basis of our analysis, shown in table 5, we estimate that Chrysler and GM would need to have a market capitalization of $54.8 billion and $66.9 billion, respectively, for Treasury to earn enough on the sale of its equity to break even. A recent Congressional Oversight Panel report reached similar conclusions on what the companies would have to be worth. As a point of reference for these values, in 1997, the last year Chrysler was a publicly traded company, its market capitalization value ranged between $23.1 billion and $31.7 billion, and in 1998, when it merged with Daimler, it was valued at an estimated $37 billion. GM, at its peak in 2000, had a market capitalization of $57 billion. In commenting on a draft of this report, Treasury officials noted that the companies’ past equity values are not comparable to today’s equity values because the companies have substantially restructured their balance sheets through bankruptcy. Although we recognize the changes the companies have experienced in recent years, we believe this information provides a sense of the magnitude of growth that will be required of the companies.

Incidentally, “table 5” looks like this:

Not good. If Chrysler builds a 40mpg car or a new engine in the US, they’ll take on more of Chrysler’s worthless equity. Win-win there (depending on your perspective). GM, on the other hand presents a bigger challenge. $66.9b market cap? In eight months? All together now, nevergonnahappen. But wait, there’s a caveat for that!

However, these estimates do not take into account other benefits and costs that are more difficult to measure, such as the impact of Treasury’s investment on jobs and local and national economies and the opportunitycosts Treasury incurred in providing financial assistance. The impact on the economy is difficult to measure because, according to the Council of Economic Advisors, it involves predicting what employment and economic performance would have been without government investment.

Finally, there’s another important wrinkle to consider:

Transparency as to how the companies are being monitored also will be important to ensuring accountability and providing assurances that the taxpayers’ investment— including both the loans to and equity in the companies—is being appropriately safeguarded. While we recognize that not all information that the companies report to Treasury should be made public because of concerns about disclosing proprietary information in a competitive market, Treasury’s approach for evaluating the success of the AIFP should be as transparent as possible, given the large taxpayer investment.

The upshot of the GAO report: there is no plan, and there’s lots of political will to ignore taxpayer value. Who saw that coming?

More by Edward Niedermeyer

Comments

Join the conversation

So, calm down. Compared to what’s been “wasted” in Iraq and Afghanistan, the $$$ sent to Motown have been chicken feed. I don't consider the liberation of millions of people to be a waste, unlike the "liberation" of billions of our tax $$ going to GM and Chrysler.

Farago's right. This was a boondoggle from jump-street. We ain't gonna see penny 1.... What this was, was a higher form of unemployment compensation for the GM, Chrysler and auto suppliers, very expensive, and with full benefits, paid for by taxpayers, bondholders and stockholders. A TraveShaMockery of the purest ray serene.... Since there really was no plan going in, other than "keep the patient alive"....why should we expect a plan to "nurse the patient back to health"? It can't be done. GM is like Tar Baby to the government. What legislator or Presidential advisor is gonna think they have the political capital, much less the will, to stand up and say "pull the plug on GM."?