Hammer Time: The Black Pawn

100 Cars are lined up for next week’s sale. Every single one of them is a repo from a very successful title pawn company… and every one has a story to tell.

The histories on many repos really begin with the license plates. Disabled Veteran… Educator… it’s amazing how many cars and trucks were once owned by folks who really made a difference in this world.

It doesn’t matter though. After 25 percent monthly interest rates and numerous attempts to get their clients to borrow even more money… their car is now forfeit. And so is their freedom.

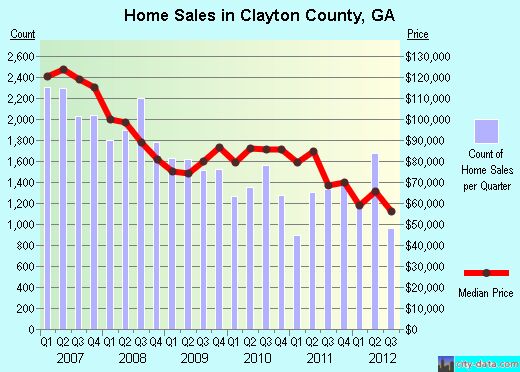

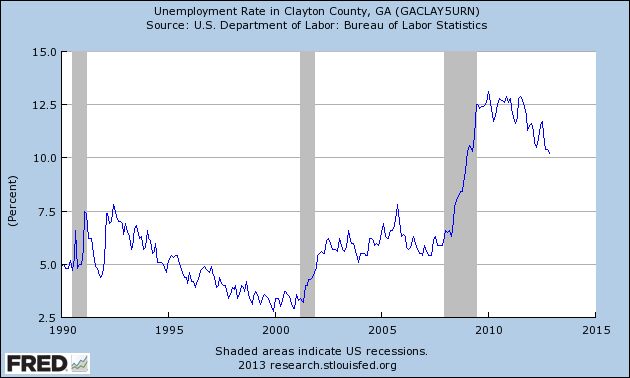

The auction will be taking place in Clayton County, Georgia. A community that is an amazing microcosm of black America. The malls are in decline. Jobs are scarce, and big box stores that were once rare to non-existent in the community are now all over the place.

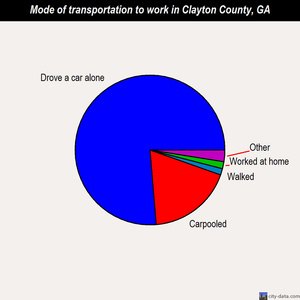

But to get to any of them you need a car. Any vehicle will do. The county has no more public transportation and the tax base continues to be affected by numerous factors.

One of them is the laissez-faire attitude towards companies that prey on the poor and the desperate. A 25 percent monthly interest rate for three months, offered by virtually every title pawn in every corner of this community, can easily compound to a loan that is too difficult to pay for those who are already struggling.

Even if that loan is only based on a 40 percent wholesale Black Book Value for the vehicle (which is typical), a $1000 loan will stay at $1000 only so long as the debtor is able to pay $750 within those first three months.

A loan default usually results in a repossessed car that can be worth many more times the original loan value. Interest payments, repo fees, administrative fees, and the inevitable auction expenses often result in a healthy profit for the title pawn company. They also result in destitution for the borrower. In Georgia you can offer a loan at a rate of over 180 percent a year. 25 percent for each of the first three months and 12.5 percent for every month thereafter… and in perpetuity.

Most states and communities outright ban title pawns due to the corrosive impact such usurious loan rate can have on the community. Wisconsin is the latest state to regulate the interest rate to a still semi-usurious 5 percent a month. That measure took years and a very tough battle with an army of highly paid title pawn lobbyists.

But other Americans (mostly in the South and Midwest) are not nearly that lucky. In some towns the number of title pawns on the main strip can outnumber the fast food joints and closed down mom-and pop businesses. The temptation is always there. Especially if there is no other financial recourse. The impact this has on our economy is far greater than one can imagine.

Any American without a car is very limited in their ability to find employment, and this reality costs money for everyone.

Taxpayers pay for more unemployment benefits and with fewer Americans able to afford a home, uncollected property taxes go up as well.

Editor’s Note:A summary of taxes receivable in Clayton County, Georgia as of June 30, 2011 is as follows:

The government has to provide more welfare services for these citizens. More debt is inevitably issued by all levels of government to pay for it all.

With more debt come interest payments and even less money over the long-term to cover deficits that are now rising dramatically. But there’s an even more depressing and sinister side to it.

That is growth. Folks who were once successful need to be able to build on those once firm foundations, and without a car, that just isn’t going to happen.

The handshake and the face-to-face time most small businesses need to get going simply can’t happen when their car is in a repo lot instead of a driveway. Neither can they easily care for their families. It’s a vicious cycle of keeping people in poverty, and in a place like Clayton County, it represents a new American reality.

The question is obviously… What to do? You can ban title pawns outright. With all the debate about free enterprise, it’s interesting to note that certain businesses that are seen as parasitic can actually do a lot of good. It’s estimated that well over 100,000 vehicles will be repossessed by title pawn companies this year.

But hundreds of thousands of Americans will also be able to pay off those loans. Should they be banned? Regulated? Left to the vagaries of the market?

Most states have chosen to ban title pawns, or to regulate them to a degree where the interest rate is far lower than the 187.5 percent annual interest rate currently charged in Georgia. In private conversations with title pawn managers, I have been told that many of these firms can usually enjoy gross profit margins that are well in excess of the amount loaned. This may be one of the reasons why a place like Clayton County is filled with title pawns while the overall employment and home ownership rates continue to decline in economically depressed communities.

Then there is the issue of local favoritism. The local title pawn auction I mentioned earlier was illegally operating in Clayton County for nearly eight months. Over a dozen auctions of approximately 700 vehicles took place with no business license, no permanent office or phone at the location, and no voice recording of the three bids required by state law to liquidate the cars. Ironically enough, it took place in the back of a closed down GM dealership that once had employed hundreds of people over the past decade.

Even after they were warned about their activity byan official the prior year, they continued to liquidate cars, the law be damned. Eventually someone informed the county of the activity and the place was shut down.

After over a dozen illegal sales and that second visit by a county official, something truly unexplainable happened.

They got their business license. It’s amazing that any business with such a long history of illegal activity would be so quickly accommodated. The neighboring City of Morrow, which had been the prior home for that auction before it was discovered, threw them out. In fact, the location of the auction had been moved three times once it came to Clayton County.

So how can anyone justify the issuing of a license in light of this? Would an unlicensed driver or struggling business anywhere be given the same treatment?

There are a lot of responsible citizens throughout our communities who try to provide for their families. In their work, and in their dealings, they pursue an opportunity to build a better life. As Americans celebrate Independence Day, the question that must be considered is whether the poor, tired and huddled masses of generations past would have sacrificed it all had they known that our government would so easily whore itself out to the powers that be?

It is a question worth considering…

More by Steven Lang

Comments

Join the conversation

An excellent and eye-opening article. Have things improved somewhat in Clayton County since this article was first written? BTW this article reminded me of one that I read on huffpost a few months ago. "Unemployment Problem Includes Public Transportation That Separates Poor From Jobs" by Peter Goodman - http://www.huffingtonpost.com/2012/07/11/unemployment-problem-public-transportation_n_1660344.html

How is this different from any pawn shop? They function the same way with other consumer items, but with cars it's somehow different?